“The US Dollar is our currency, but it’s your problem” – John Connally, Secretary of the Treasury of President R. Nixon, G10 Meeting, Rome, Italy 1971

Despite declining by more than 10 percent against major currencies since the onset of the Pandemic, the US Dollar seems to be stuck in the crosshairs of the bears and doomsayers, undermined by a massively deteriorating fiscal position and an ever-accommodative monetary stance no longer concerned with price stability (i.e., the “new” Average Inflation Targeting policy stance.) The new Administration of President Biden is exploiting further the fiscal lever and has announced as its first major policy initiative a US$ 1.9 Trillion program, thus adding further to anxieties of an ever-growing US public debts.

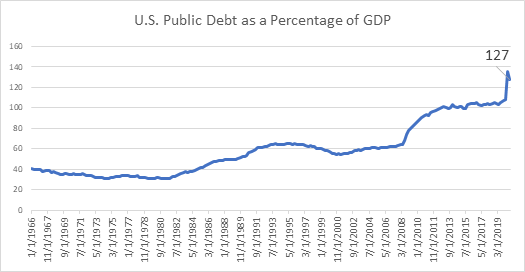

Indeed, the ratio of debt to GDP rushed through the crucial level of 100 percent following the unfunded tax cut of 2017 and is supposed to reach 135 percent by 2025 according to the IMF (See Fig. 1).

Figure 1: Federal Debt: U.S. Public Debt as a Percentage of GDP

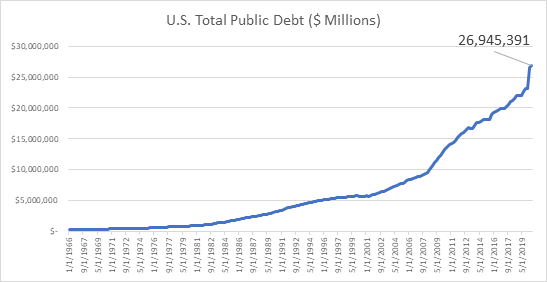

While these levels for the ratio are now a common global phenomenon across the developed and emerging world, the actual dollar amount of US debt that needs to be absorbed out there (See Fig. 2) coupled with a never-ending QE, increases the risks, according to some, of a debasing of the currency ending up in a crash[1]. We disagree … one must distinguish between the Role of the Dollar and the Value of the Dollar, two entirely different analyses: The Role of the dollar has defined very sturdy and insuperable guardrails within which the currency will periodically move reflecting “normal” economic and financial drivers. Accordingly, we believe that the ~ 10 percent decline in the index value of the US Dollar (DXY) reflects “normal” fluctuations reflecting underlying economic and financial factors and is definitely not a precursor of a crash, far from it!

Figure 2: Federal Debt: U.S. Public Debt

The Role of the US Dollar

In the World Financial Order, the US dollar is the Sun … everyone else rotates around it. It would take an act of the All-Mighty to change this well-established state of affair … and creating a crash!

The aftermath of WWII left most of the world in shatter, except to some extent the United States. Thus, the Bretton Woods Conference which established the new world financial order set a system of payments based on the US currency, whereby the exchange rate of each participating currency would be pegged against the dollar which in turn would be freely convertible into gold. The system worked relatively well until August 1971, when, forced amongst other things by substantial pressure on US gold reserves, President Nixon announced the end of the convertibility of US Dollar in gold. Less than two years later in March 1973, the G–10 approved an arrangement whereby six members of the European Community tied their currencies together and jointly floated against the U.S. dollar, a decision that effectively signaled the abandonment of the Bretton Woods fixed exchange rate system in favor of the current system of floating exchange rates. To most pundit, that was supposed to be the beginning of the end of the Mighty Dollar.

Well, fifty years later or a full half a century, the US currency still reigns unopposed. To start with, the dollar remains the currency of choice to invoice global trade as trading in the same “global” currency of global trading partners obviously reduces foreign exchange transaction costs and liquidity risks. The result is that, of the US$ 6.6 trillion of daily foreign exchange transactions, close to 90 percent are transactions against the US currency. This in turn requires and feeds off a deep and complex US capital market, with a financial infrastructure virtually unmatched by any other market in size and scope … and further endorsed by a dynamic economy, outstanding research institutions, innovative corporate sector, a well-educated and productive labor force … not to mention sturdy institutions and a colossal global military presence.

Indeed, and despite the very recent profoundly serious trials and tribulations, the US Judiciary Institutions have withstood the test of time and reliability, thus providing a necessary condition for the haven status of the dollar. As a result, and despite occasional competition (e.g., the Euro), the US Dollar is still about two-thirds of global official reserves. I.e., there does not seem to be any serious alternative to the global role of the US Dollar. In fact, during the fifty years since the breakup of the Bretton Woods exchange rate system, anytime the dollar run into “trouble” threatening the status quo in the global financial system, the rest of the world mobilized quickly and gladly came to its support giving total credence to Secretary Connolly’s quip: “the dollar is our currency, but it’s your problem!”

The Value of the Dollar

Nonetheless, the global role of the dollar does not shield the currency from standard economic and financial drivers determining its value in the marketplace. To that end, the dollar is subject to entirely normal fluctuations as has been the case recently. Sure enough, after a brief but sharp (~8%) appreciation during the onset of the Pandemic in March 2020 and reflecting its haven status, the dollar has been in a relentless decline, depreciating by ~ 13 % from peak to trough (See Fig. 3) below reflecting the aggressive and super accommodative reactions of the US authorities to the pandemic damages.

Figure 3: The Fall of the DXY (Dollar) Index

The Monetary Driver

To start with, the “normal” driver behind the sizeable move was the expectation that interest rate differentials in favor and recently sustaining the US Dollar relative to major currencies (i.e., the Euro) was going to be wiped out following the aggressive accommodative measures of the Federal Reserve, i.e., cutting short term rates to zero and further increasing QE (purchasing bonds in the marketplace) by a staggering US$ 700 billion, thus further widening an already ballooning balance sheet.

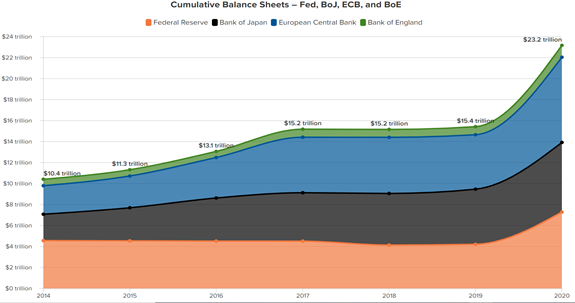

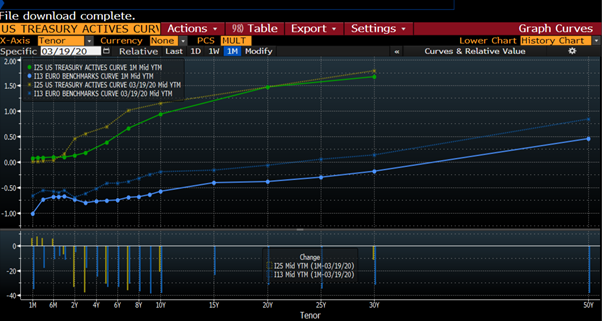

While the market reaction has been initially justified, the yield differential stop narrowing and now seems to be well on its way of reversing back in favor of the US Dollar as illustrated in Fig. 4 below. In addition, there is no reason let alone evidence that the Federal Reserve QE will be more aggressive than other major central banks (See Fig. 5 below). Lastly, and despite the sharp movement in the spring of 2020, the relative shape of the yield curves in the U.S. and Europe, or another reliable medium-term driver of currency movement, have hardly changed, as illustrated in Fig. 6. Accordingly, the interest rate differential of the US Dollar versus major currencies is no longer a reason to expect a further decline in the currency in our view … on the contrary!

Figure 4: Interest Differential between US 10-year Govt and EURO 10-year Govt

Figure 5: Cumulative Balance Sheets of Major Central Banks

Figure 6: Yield curves of US vs. Europe (January 19, 2021 vs. March 19, 2020)

The Fiscal Driver

The role of fiscal policy appears to have been a much stronger driver of exchange rate movements lately, possibly considering the sheer size of (now) periodical major fiscal packages implemented across major countries. Indeed, as illustrated in Fig.7, the driver behind the major movement in the dollar in 2017 was probably the unfunded 2017 Tax cut, thus adding a then staggering US$1 trillion to the federal debt. The same can be inferred for 2020, following the announcement of the US$ 2.2 Trillion CARES Act, a massive effort relative to other individual countries. In both cases, the fiscal action seems to be the prime catalyst of the US Dollar decline.

Figure 7: Trend of DXY (Dollar) Index since 2016

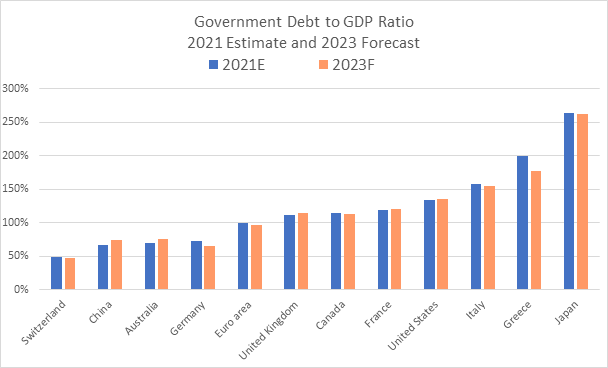

Now, despite the recent proposal of a US$ 1.9 Trillion package by the Biden Administration, the US fiscal stance is not different from and is at par with major economic blocks fielding similar fiscal policies to cope with the economic and health ravages of the Pandemic. Indeed, in December 2020 the European Union announced a Euro 1.8 Trillion (US$ 2.2 Trillion), the largest stimulus package ever financed through the Union budget … a historical achievement for a political block that has so far refused to set up a fiscal union! Not to mention Japan, where public debt over GDP had reached a stunning level even before the Pandemic, i.e., 250% and counting! Indeed, as Fig. 8 shows, the US fiscal position is far from being the worst across major countries and is very much in line with the “new fiscal normal”, i.e., there should not be any unusual pressure on the US dollar because of it.

Figure 8: Estimated Debt to GDP Ratio for Major Countries

The External Driver

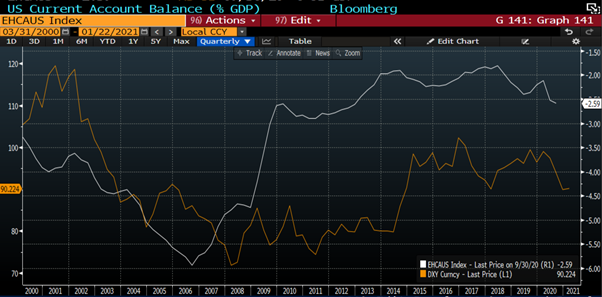

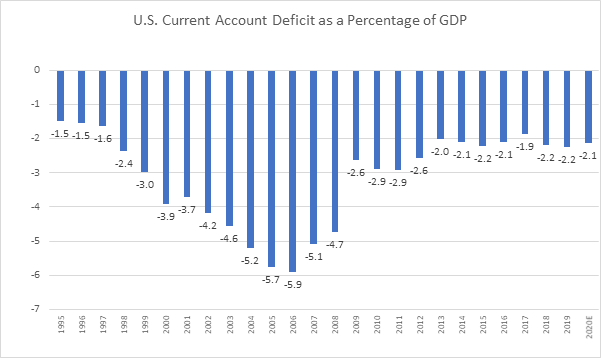

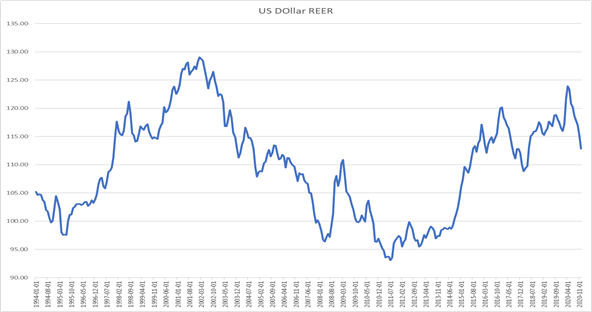

Last (for this note) but not least, the external trade position will both reflect and impact the level of any currency. To that end, the US dollar is no stranger to periodical pressures arising from the US external trade positions, Fig. 8 below very clearly illustrates this cause and effect at least for the last twenty years. Possibly reflecting an ever-widening current account deficit from 2000 onwards, the dollar began to decline against major currencies until 2008, and sure enough, the external position began to correct from 2007 onwards. Since then, and as further illustrated by Fig. 9 and Fig. 10, the US external position seems to have stabilized at around 2.5 percent of GDP, a far better external position relative to the peak external deficit of 2006 and possibly reflecting the slight strength of the US Dollar as measured by its Real Effective Exchange Rate, or the crucial index of external competitiveness (see Fig. 11). Hence, here too we do not see any reason to be alarmed, let alone fearing a crash in the US dollar.

Figure 9: U.S. Quarterly Current Account Balance as a Percentage of GDP vs. Dollar Index

Figure 10: U.S. Yearly Current Account Deficit as a Percentage of GDP

Fig. 11: U.S. Dollar Real Effective Exchange Rate

Conclusion

One of the most humbling experiences of our job has been by far to attempt to forecast exchange rates. Nonetheless, there are good reasons to expect that over the long term, all currencies will eventually reflect fundamentals and will not stray away from their intrinsic value … the keyword here is eventually! Accordingly, and based on our estimates of value, we believe that the recent dollar correction against major currency is pretty much done, and, in any case, far from being on the verge of a crash as peddled by some pundits!

Having stated the above, we also must confess that we rarely try to “make money” out of our call on the US Dollar. Instead, we fall in the camp believing that correctly predicting the direction of the US currency has much more value as a core element in assessing the global investment environment and making more informed investment decisions. That is the US Dollar has yet another well recognized “tactical role” as an index of global investment sentiment, i.e., a weaker to stable dollar is always part and parcel, a feature, and a condition of an upbeat global investment outlook, or what nowadays is most commonly known as risk-on!

Lumen Global Investments, San Francisco, January 2021

[1] See “Is a Dollar Crash Coming?”, a Symposium of Views. The International Economy, Fall 2020